Small doubt in two articles

(This post is a little bit dated now, because I made a first draft last week. But anyway I'll post it below.)

I've got a small doubt in two articles (Washington Post, Bloomberg) that I found on Abnormal Returns, which compactly summarized them as

First of all, I'm not intending to blame Abnormal Returns. It only summarized two articles into one sentence. That's it.

I have a problem in each of two articles.

Let's see a consumer's side, first.

Washington Post claims that

But at the very moment, Americans resumed borrowing again, and savings rate is slightly declining. In fact, consumer credit compiled by the Fed increased for three consecutive months, the first time since the mid 2008. Moreover, savings rate declined to 5.3% in December, a nine-month low since last May. As the economy turns up, Americans have stopped a thrift life, and returned to the "good old days", though it's very modest compared to the housing bubble period in the early 2000's.

Second, while no one denies that corporations has just started spending again in the US, Bloomberg's reason is questionable.

In my opinion, it's a mysterious theory that companies expand capital spending because the President pleads. If so, the President could readily manipulate the economy through corporate spending in his favor, especially just before the election. It looks like the US is a communist, dictatorship nation.

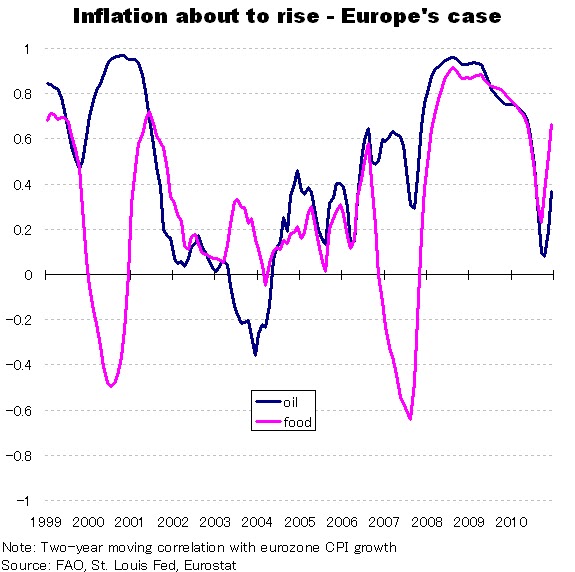

The fact is, I think, that companies build up investments because the stock market, hence economic prospect, rises.

Look at the graph above, and you'll find that the stock market has a positive correlation with corporate investments. A democratic, capitalist society wouldn't be easy for corporations to increase spending even if it's the President's order.

I've got a small doubt in two articles (Washington Post, Bloomberg) that I found on Abnormal Returns, which compactly summarized them as

Consumers are reducing indebtedness while corporations begin to spend their cash hoards.Is that really so?

First of all, I'm not intending to blame Abnormal Returns. It only summarized two articles into one sentence. That's it.

I have a problem in each of two articles.

Let's see a consumer's side, first.

Washington Post claims that

Climbing out of debt, Americans are saving moreNot bad as a start. Then, a story goes on.

The recession that just rocked the U.S. economy happened in part because Americans were borrowing and spending more than they could afford. Now, three years after the downturn began, families are moving faster than many analysts had expected to put their finances in order by paying down debt and boosting their savings.

Compared with the summer of 2008, when consumer debt peaked, Americans now have 7 percent less mortgage debt, 12 percent less in auto loans and 15 percent less credit card debt, according to the Federal Reserve Bank of New York. Loan payments last year were at their lowest level in a decade.It's true that Americans have slashed spending, payed loans back, and increased savings since the financial meltdown in 2008, which has so far curtailed several million jobs.

Meanwhile, Americans are saving at nearly triple the rate they did between 2007 and 2009, setting aside 5.3 percent of their disposable income in December, according to the Commerce Department.

But at the very moment, Americans resumed borrowing again, and savings rate is slightly declining. In fact, consumer credit compiled by the Fed increased for three consecutive months, the first time since the mid 2008. Moreover, savings rate declined to 5.3% in December, a nine-month low since last May. As the economy turns up, Americans have stopped a thrift life, and returned to the "good old days", though it's very modest compared to the housing bubble period in the early 2000's.

Second, while no one denies that corporations has just started spending again in the US, Bloomberg's reason is questionable.

Corporate America is putting its cash hoard back to work.Really? Are you sure?

In the first decline since mid-2009, Standard & Poor's 500 companies reduced cash and short-term investments to $2.4 trillion from a record $2.46 trillion, according to data Bloomberg compiled from their most recent quarterly reports. Capital spending increased $22.3 billion, the biggest quarter- to-quarter jump since the end of 2004, to $142.8 billion, the highest level in two years.

Budgets are rising for new plants, distribution centers and stores from S&P bellwethers Cisco Systems Inc., General Electric Co. and Coca-Cola Co. While some of the money is being spent abroad, company officials say they are opening the purse strings at home now too. A rebound in economic demand, President Barack Obama's efforts this year to court business leaders, and Republican gains in Congress have helped build confidence to invest and start adding jobs, executives and investors said.

In my opinion, it's a mysterious theory that companies expand capital spending because the President pleads. If so, the President could readily manipulate the economy through corporate spending in his favor, especially just before the election. It looks like the US is a communist, dictatorship nation.

The fact is, I think, that companies build up investments because the stock market, hence economic prospect, rises.

Look at the graph above, and you'll find that the stock market has a positive correlation with corporate investments. A democratic, capitalist society wouldn't be easy for corporations to increase spending even if it's the President's order.

Labels: US

posted by Akihiro Gotoda at

2:23 PM

0 Comments

![]()