BoJ's cause

Nobody expected anything important to be announced at the Bank of Japan's monetary policy meeting yesterday, but one thing looks like worth mentioning. The BoJ, as expected, held its key policy interest rates unchanged at 0 to 0.1%, and unveiled the details of "comprehensive monetary easing" put forth in early October, including the purchase of low-graded corporate bonds.

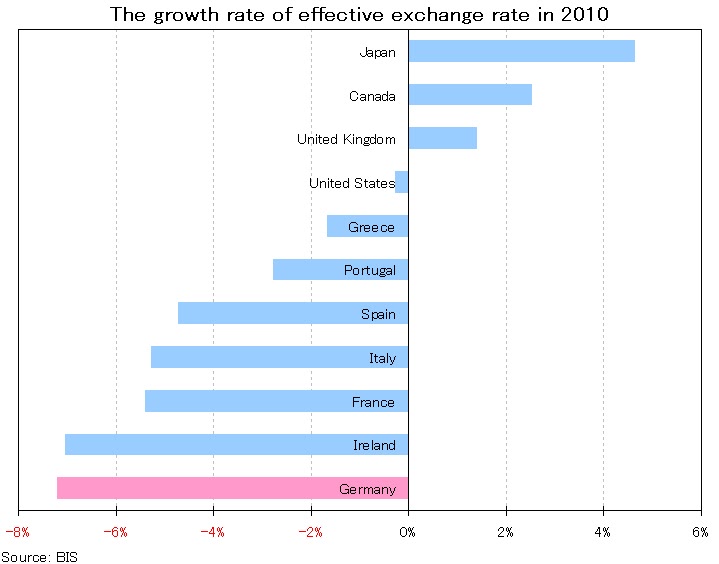

One has to notice, however, that the Japanese central bank moved up its next meeting to November 4-5, which was originally scheduled to be held in November 15-16. The BoJ said the reason for change is "to discuss and decide the principal terms and conditions for the purchases of ETFs and J-REITs with a view to promptly starting their purchases." But given that the Fed is likely to start QE2 at the FOMC meeting in November 2-3, it should be read that the BoJ's true intention is to make a quick response to prevent the yen from appreciating further after the Fed's additional monetary policy easing, probably adding another round of bond purchase.

Coincidentally, both the Bank of England and European Central Bank will announce the result of their monetary policy meeting in November 4. But their position is different from the BoJ's, and they wouldn't consider the Fed's policy as too critical to be factored in their monetary policy decisions.

First, Britain's third quarter GDP beat market expectations by a wide margin, and S&P has just changed its outlook for Britain's long-term sovereign bond from negative to stable, which by no means hastens the BoE's policy change at this time.

Second, Germany is estimated to grow by more than 3% this year due to weak euro, placing itself as one of the fastest growing economies among rich nations. The ECB would feel content as Europe's largest economy is in a good shape, though having fiscally feeble countries like PIIGS yet.

BoJ's cause, though covert, is distinct from its peers in that it has to take strengthening currency as detrimental to a deflation-riddled, debt-overloaded and export-dependent country.

One has to notice, however, that the Japanese central bank moved up its next meeting to November 4-5, which was originally scheduled to be held in November 15-16. The BoJ said the reason for change is "to discuss and decide the principal terms and conditions for the purchases of ETFs and J-REITs with a view to promptly starting their purchases." But given that the Fed is likely to start QE2 at the FOMC meeting in November 2-3, it should be read that the BoJ's true intention is to make a quick response to prevent the yen from appreciating further after the Fed's additional monetary policy easing, probably adding another round of bond purchase.

Coincidentally, both the Bank of England and European Central Bank will announce the result of their monetary policy meeting in November 4. But their position is different from the BoJ's, and they wouldn't consider the Fed's policy as too critical to be factored in their monetary policy decisions.

First, Britain's third quarter GDP beat market expectations by a wide margin, and S&P has just changed its outlook for Britain's long-term sovereign bond from negative to stable, which by no means hastens the BoE's policy change at this time.

Second, Germany is estimated to grow by more than 3% this year due to weak euro, placing itself as one of the fastest growing economies among rich nations. The ECB would feel content as Europe's largest economy is in a good shape, though having fiscally feeble countries like PIIGS yet.

BoJ's cause, though covert, is distinct from its peers in that it has to take strengthening currency as detrimental to a deflation-riddled, debt-overloaded and export-dependent country.

posted by Akihiro Gotoda at

11:58 PM

0 Comments

![]()